Archive for November 2016

Mortgage approval isn’t final until it’s funded. Things can change prior to the loan being closed that can affect a pre-approval such as changes in the borrowers’ financial situation or possibly, factors beyond their control like interest rate changes.

Good advice to buyers is to do nothing that can affect your credit report until the loan closes. Opening new credit cards, taking on new debt for a car or furniture or changing jobs could affect the lender’s decision if they believe you may no longer be able to repay the loan.

The benefits of buyer’s pre-approval are definitive: it saves time, money and removes the uncertainty of knowing whether the buyer is qualified. The direct benefits include:

- Amount the buyer can borrow – decreases as interest rates rise

- Looking at “Right” homes – price, size, amenities, location

- Find the best loan – rate, term, type

- Uncover credit issues early – time to cure possible problems

- Bargaining power – price, terms, & timing

- Close quicker – verifications have been made

It is a very common practice for mortgage lenders to require income and bank verifications and to re-run the borrowers’ credit one final time just prior to closing. Mortgage approval isn’t final until it’s funded.

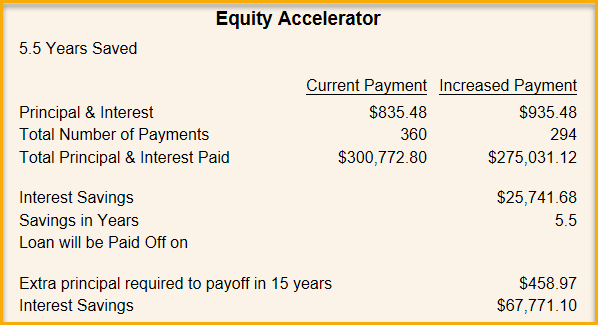

Most people think they’ll have a house payment and a car payment for the rest of their lives but it doesn’t have to be with a plan and a little discipline. The plan is to make additional principal contributions to a fixed rate mortgage to shorten the term and save tens of thousands in interest.

If a person were to make an additional $100 payment each month applied to principal on a $175,000 mortgage, it would shorten the loan by five years six months. If the person were to make $200 a month additional payments, it would shorten the loan by 9 years. $459 additional payment would shorten it to 15 years.

If a person does make a decision to regularly pre-pay their mortgage, it will be their responsibility to verify that the lender is applying the money to the principal each time as opposed to being placed in the reserve account for taxes and insurance.

In today’s market, a savings account pays around 0.5% or less. Even with the low mortgage rates available, there is still a considerable savings. People who might need the funds in the near future should carefully consider this option due to the difficulty to access equity easily from one’s home.

Make your own projections using the Equity Accelerator.

Homeownership, part of the American Dream: a home of your own where you can feel safe, raise your family, share with your friends and enjoy life. The benefits are easily recognizable but maintenance is just as real and should be considered.

Property taxes and insurance are two of the largest expenses homeowners have aside from their mortgage interest. But, as any homeowner knows, there will be occasional expenses for repairing toilets, faucets, windows and other things. There are also the significantly larger expenses that arise like replacing a water heater or HVAC unit. And don’t overlook the periodic maintenance like painting or floor coverings.

Financial experts suggest that homeowners save one to four percent of the home’s value per year for repairs and maintenance. Two to eight thousand dollars a year may sound like more than you’ll need but the cost of an air conditioning unit can easily be $6,000 and some homes have more than one unit, which hopefully, won’t need to be replaced in the same year.

Some homeowners purchase home warranties to avoid the unexpected costs. An annual premium instead of an unexpected large expenditure. Coverage varies from company to company and are not intended to cover existing conditions.

The alternative to not saving for these anticipated expenditures means that a homeowner might have to put it on a credit card at a very high interest rate or get a home improvement loan. Appreciation is a distinct benefit of home ownership and deferred maintenance can limit the value as well as lengthen the market time when it sells.

There is certainly no shortage of retirement planning strategies available to individuals who actually take the time to consider them. What most financial experts do agree on is that the closer you are to retirement, the less time you have to recover from a loss. For that reason, many people start dialing down their risk factors as their age increases.

One way to minimize risk is to invest in things that you know and understand. For the majority of homeowners, their largest asset is the equity in their home which they generally have more familiarity than other types of investments.

One way to minimize risk is to invest in things that you know and understand. For the majority of homeowners, their largest asset is the equity in their home which they generally have more familiarity than other types of investments.

Buy the home you’d like to retire to today and use it as a rental property. Finance it with a 15 year loan so it will amortize quickly and possibly be paid for at retirement.

Continue living in your current home until you’re ready to move into the home you’ve designated at your retirement home which will not create a taxable event. Prior to moving in, you can rehab the home so that it fits your style and needs exactly.

If you’ve lived in the current home for at least two of the last five years, you can exclude up to $250,000 of gain for single taxpayers and up to $500,000 for married taxpayers. The proceeds could then, be invested for income.

Some of the attractive features of this proposal is that you’re familiar with the operation of a rental due to similarity of owning a home. Most experts agree that home prices will continue to rise and so will rents. The maintenance people that you use for your home can also work on your rental. If you don’t want to deal with tenants that can easily be delegated to a property manager. Low mortgage rates with short terms and high rental values contribute to positive cash flows that will pay for the property.

Obviously, there are many other considerations you’ll want to investigate with your tax and real estate professionals these can get the conversation started.